Vert Global Sustainable Real Estate Fund (VGSRX)

Fund Commentary

June 30, 2023

| For the period ending June 30, 2023 | 1 Month | 3 Month | YTD | 1 Year | 3 Year | 5 Year | Since Inception 10/31/2017 |

|---|---|---|---|---|---|---|---|

| Vert Global Sustainable Real Estate Fund | 4.35% | 1.79% | 1.90% | -3.84% | 4.30% | 0.53% | 0.80% |

| S&P Global REIT Index | 3.11% | 0.71% | 2.09% | -3.02% | 5.34% | 1.35% | 1.89% |

Performance data quoted represents past performance and does not guarantee future results. Investment returns and principal value will fluctuate, and when sold, may be worth more or less than their original cost. Performance current to the most recent month-end may be lower or higher than the performance quoted and can be obtained by calling 1-844-740-VERT. Investment performance reflects fee waivers in effect. In the absence of such waivers, total returns would be reduced. Short term performance, in particular, is not a good indication of the fund’s future performance, and an investment should not be made based solely on returns. Return figures over 1 Year are annualized. The fund Gross Expense Ratio is 0.67%. The fund Net Expense Ratio is 0.50% via expense limitation. Contractual fee waivers through October 31st, 2025. The net expense ratio applies to investors.

Second Quarter 2023 Update

- The Fund attracted $27 million in net new assets in the second quarter, taking YTD flows to $112 million.

- AUM has risen from $175 million at year end to $291 million as of June 30, 2023.

- In this quarter’s Spotlight we examine “Climate Change Comes for Home Insurance”.

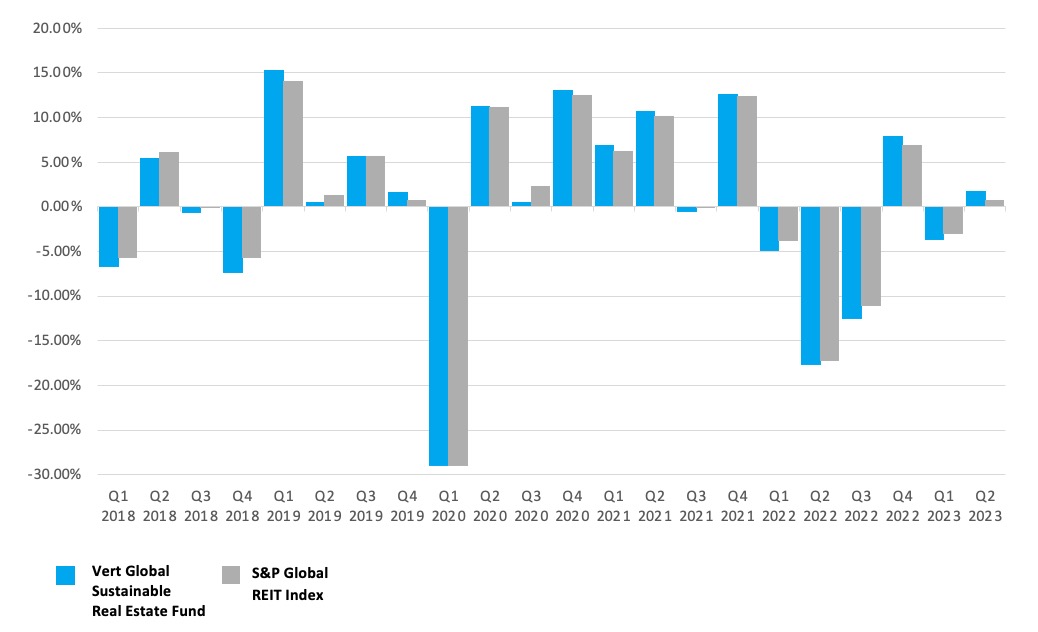

Performance

A strong return of 4.35% in the month of June brought the quarter and the year-to-date performance into positive territory. The economy continues to prove more resilient than many had feared, and inflation seems to be tapering for now. Nevertheless, investors remain concerned about interest rates and inflation, thus keeping equity volatility high.

Positive returns for the year so far suggest that investors may be realizing that REITs are, for the most part, resilient to interest rate hikes. Most REITs, with some notable exceptions of course, have fixed-rate long-term debt. Rising interest rates do increase costs but the bulk of these higher expenses will not be incurred for several years. Meanwhile REITs can raise rents more than usual given the inflationary environment. Returns may remain volatile while the Fed considers further rate hikes.

Despite the volatility in real estate markets, the Fund continues to deliver returns similar to the benchmark. Most quarters see returns for the Fund within about 1% of the benchmark.

For most of the Fund’s existence, and for each of the last 11 quarters, the Fund has outperformed the benchmark in positive returning quarters and underperformed in negative ones. This higher ‘beta’ is to be expected as the Fund holds less than 150 companies while the S&P Global REIT Index holds over 400.

We are very comfortable with this type of performance. It is our expectation that markets rise over time. If this pattern of performance persists over the long term, where the Fund beats the Index in positive markets, comparative performance to the benchmark should be good as markets return to form.

AUM and Fund Flows

The Fund had its second-best quarter ever for net flows, attracting over $27 million in new assets. The year-to-date total of $112 million more than doubles lasts year’s 12-month total of $52 million.

Spotlight on “Climate Change Comes for Home Insurance”

After the particularly devastating wildfires in Northern California in 2020, some of our neighbors in the Bay Area found it difficult to renew their home insurance policies. Their situation was not uncommon. Between 2015 and 2021, over 1.3 million Californians had their fire coverage dropped by an insurer, out of a total of around 10 million total polices in the state, according to data gathered by the California Insurance Commissioner’s office.1 Perhaps these insurers had had enough – wildfires have caused more than $30 billion in insured losses in California since 2017, according to the reinsurance company Munich Re.2

Climate change doesn’t start wildfires; lightning, aging powerlines, and arsonists do. But the extended droughts and high temperatures that climate change exacerbates makes the fires more intense, more destructive, and much harder to put out. The risk profile of a home in California is now higher due to climate change. Unfortunately, it’s not just in California.

Farmers Insurance recently announced it will stop writing new business and not renew existing automobile, home and umbrella policies in Florida. The company’s official statement said, “This business decision was necessary to effectively manage risk exposure”. Makes sense – Hurricane Ian caused over $60 billion in insured losses by itself.3

Where Insurers are Exiting Markets

More property owners will be finding it difficult to insure their homes and businesses going forward.

- Florida

- Farmer’s departure is just one of many recent terminations. In the last 18 months, 7 Florida property insurers were declared insolvent and another 15 have stopped writing new business.4

- Farmer’s departure is just one of many recent terminations. In the last 18 months, 7 Florida property insurers were declared insolvent and another 15 have stopped writing new business.4

- California

- State Farm recently announced it would stop accepting applications for all business and personal lines of property and casualty insurance, citing inflation, a challenging reinsurance market and “rapidly growing catastrophe exposure.”

- Allstate, another insurance powerhouse, announced in November 2022 it would pause new homeowners, condo and commercial insurance policies in California to protect current customers. “The cost to insure new home customers in California is far higher than the price they would pay for policies due to wildfires, higher costs for repairing homes and higher reinsurance premiums,” Allstate said in a statement.5

- Colorado

- In Colorado, which has also been hit by devastating wildfires, insurance premiums have been rising significantly, and some smaller insurance companies have been pulling back from covering properties. A study commissioned by state lawmakers found that 76% of carriers decreased their exposures in Colorado in 2022, leaving the five largest insurance companies to dominate the market.5

- In Colorado, which has also been hit by devastating wildfires, insurance premiums have been rising significantly, and some smaller insurance companies have been pulling back from covering properties. A study commissioned by state lawmakers found that 76% of carriers decreased their exposures in Colorado in 2022, leaving the five largest insurance companies to dominate the market.5

- Louisiana

- Louisiana is in the middle of a property insurance crisis. This summer alone, nine insurance companies that wrote homeowners policies in the state have gone belly-up since a series of hurricanes hit the state in 2020. A dozen other companies have withdrawn from the state, either by canceling existing policies or announcing they won’t renew them.6

- Louisiana is in the middle of a property insurance crisis. This summer alone, nine insurance companies that wrote homeowners policies in the state have gone belly-up since a series of hurricanes hit the state in 2020. A dozen other companies have withdrawn from the state, either by canceling existing policies or announcing they won’t renew them.6

What Happens to a Home’s Value When You Can’t Insure?

In California, you might expect to pay $1,300 a year for home insurance. Average rates like that, which are set by regulators, “have been artificially low for decades,” according to the Insurance Information Institute (III). California passed a resolution in 2008 that barred insurers from raising rates more than 7% per year. This well-intentioned law is backfiring – now homeowners are having to go without insurance at all.

In other markets, rates are rising rapidly. In Florida, the III expects the average cost to rise 43% in 2023, reaching $6,000 per year. Some experts expect $10,000 to be the norm in just a few years.7 Still, insurers are choosing to leave. That says a lot about the actual risks in Florida.

Expensive insurance makes buying and owning a home less affordable. This reduces the pool of prospective buyers; and also reduces the overall value of properties. Many insurers will require homeowners to make costly upgrades to their homes to make them more resilient before they agree to insure it. Fire resistant roofs and storm proof windows don’t come cheap.

But even with costly upgrades, expensive insurance is better than none at all. Many homeowners will struggle to get insured with providers exiting whole states at a time. So what happens if you can’t get insurance? Well, it becomes much harder to sell. Many banks require buyers to have insurance if they want a mortgage. Without a good market of buyers, some folks might have no choice but to stay in their unsellable home. Much has been made of ‘climate refugees’ – people forced from their homes because of rising climate risks. Will we see ‘climate prisoners’ as well?

Planning for Climate Change

Even scientists who study the effects of climate change struggle to predict what changes will occur where, and when. Safe havens are increasingly hard to find – as we’ve discovered this summer, wildfire smoke can affect those that are hundreds of miles from forests.

We can change our expectations and be better prepared. Increase your expected expenses for home insurance, for renovations, and for resilience and recovery efforts. Do not assume costs to rise with the rate of inflation – think much worse. Plan for the possibility of having to self-insure.

At this point, we shouldn’t be surprised by the dramatic changes in the weather. Re-examine those holiday home or retirement destinations with an eye on what the future climate will be, not what it is today. Imagine what the true length of the golf/ski/tennis/bike season will be when temperatures are in the 90s for weeks or months at a time. Consider that some of those dream waterfront homes could turn into your worst nightmare.

DOWNLOAD

Explore more commentaries.

1 https://www.context.news/climate-risks/home-insurance-coverage-falters-as-california-wildfires-worsen

2 https://www.npr.org/2023/07/22/1186540332/how-climate-change-could-cause-a-home-insurance-meltdown

3 https://www.reuters.com/business/environment/hurricanes-floods-bring-120-billion-insurance-losses-2022-2023-01-09/

4 https://www.usatoday.com/story/money/2023/07/11/farmers-insurance-leaving-florida-market/70403832007/

5 https://abcnews.go.com/US/wireStory/california-insurance-market-rattled-withdrawal-major-companies-99855058

6 https://www.nola.com/news/business/here-are-the-louisiana-insurers-that-have-gone-broke-or-left-the-state-amid-deepening

7 https://www.axios.com/2023/06/06/climate-change-homeowners-insurance-state-farm-california-florida

Please refer to the Prospectus for full risk disclosures. All data as of June 30, 2023 and subject to change daily.

Beta is a measure of the volatility—or systematic risk—of a security or portfolio compared to the market as a whole.